In the complex world of personal finance, few numbers hold as much power as your credit score. It's a three-digit figure that can open or close doors to significant financial opportunities, influencing everything from the interest rate on your mortgage to whether you'll get that dream apartment. But amidst all the talk, a fundamental question often arises: What is a good credit score? Understanding this isn't just about knowing a number; it's about grasping a crucial pillar of your financial health.

Many people vaguely understand that a higher score is better, but pinpointing exactly what constitutes a "good" credit score can feel like a moving target. Is it 700? 750? Or something else entirely? This comprehensive guide will demystify credit scores, answer the question "What is a good credit score?" across different models, explain why it matters, and provide actionable strategies to achieve and maintain excellent credit.

Understanding Credit Scores: What is a Good Credit Score Across Different Models?

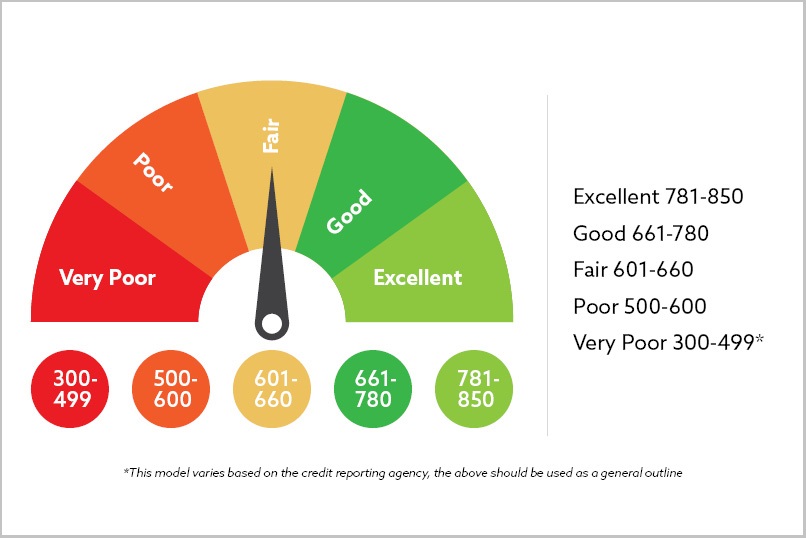

Before we define what is a good credit score, it's essential to understand that there isn't just one universal credit score. The two most widely used scoring models are FICO® Score and VantageScore®. While both evaluate your creditworthiness, they use slightly different methodologies and have varying ranges. Generally, both models operate on a scale of 300 to 850.

Here’s a breakdown of what credit score ranges typically mean for both FICO and VantageScore:

| Credit Score Range | FICO® Score Category | VantageScore® Category | Lender Interpretation |

|---|---|---|---|

| 800-850 | Exceptional | Excellent | Lowest interest rates, highest approval odds. |

| 740-799 | Very Good | Good | Very favorable terms, strong borrower. |

| 670-739 | Good | Fair | Average terms, generally approved. This is often the benchmark for "What is a good credit score?" |

| 580-669 | Fair | Poor | Higher interest rates, potential for denials. |

| 300-579 | Poor | Very Poor | Significant challenges, likely denials or very high rates. |

As you can see, for many lenders, a FICO score of 670 or higher is generally considered "good." A VantageScore in the "Good" category typically starts around 700. However, aiming for "Very Good" or "Excellent" gives you a much stronger financial standing and access to the best rates and offers. When asking "What is a good credit score?", most financial experts would point to scores in the 700s and above as truly beneficial.

Why Does Having a Good Credit Score Matter So Much?

Possessing a robust credit score isn't merely about bragging rights; it's a powerful financial tool that significantly impacts your life. Here’s why understanding what is a good credit score and striving for it is so critical:

- Lower Interest Rates: This is perhaps the most significant benefit. Lenders view individuals with good credit as less risky. This translates into lower interest rates on mortgages, auto loans, personal loans, and credit cards, saving you thousands of dollars over the life of your loans.

- Easier Loan and Credit Card Approvals: A good score increases your chances of getting approved for the credit products you need, from buying a home to financing a car.

- Better Terms on Credit Cards: You'll qualify for premium credit cards offering attractive rewards, sign-up bonuses, and lower APRs.

- Reduced Insurance Premiums: In many states, insurance companies use credit-based insurance scores (derived from your credit report) to help determine your premiums for auto and home insurance. A better score can mean lower rates.

- Easier Rental Approvals: Landlords often check credit scores as part of their tenant screening process. A strong score can give you an edge in competitive rental markets.

- Waiver of Utility Deposits: Utility companies may waive security deposits for customers with good credit, saving you upfront costs when setting up new services.

- Better Cell Phone Deals: You might qualify for better financing terms on new phones or contracts without a significant deposit.

Breaking Down the Numbers: What is a Good Credit Score Based On?

To truly understand "What is a good credit score?" you need to know what factors contribute to its calculation. While FICO and VantageScore use proprietary algorithms, they generally weigh similar categories. We'll focus on the FICO model, as it's the most widely used by lenders.

Here are the five key components of your FICO Score and their approximate weighting:

- Payment History (35%): This is the most crucial factor. Paying bills on time consistently demonstrates reliability. Late payments, bankruptcies, collections, and charge-offs significantly harm your score.

- Amounts Owed / Credit Utilization (30%): This refers to the amount of credit you're currently using compared to your total available credit. Keeping your credit utilization ratio low (ideally below 30% of your total credit limit across all cards) is vital. High utilization suggests you might be over-reliant on credit.

- Length of Credit History (15%): A longer history of responsible credit use is generally better. Lenders like to see a track record. The age of your oldest account, the average age of all your accounts, and how long specific accounts have been open all play a role.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., installment loans like mortgages or car loans, and revolving credit like credit cards) can positively impact your score. It shows you can manage various forms of debt responsibly.

- New Credit (10%): Applying for too much new credit in a short period can be seen as risky. Each "hard inquiry" (when a lender pulls your credit report after an application) can temporarily ding your score. Opening too many new accounts too quickly also shortens your average credit age.

Demystifying "Good": Is Your Credit Score Truly Good?

While the table above provides general categories, the definition of "good" can also depend on the specific financial product you're seeking. For example, a score that's "good" for getting a basic credit card might not be enough to secure the absolute lowest interest rate on a large mortgage. Lenders set their own thresholds, but a higher score always positions you more favorably.

For a mortgage, particularly a conventional loan, many lenders look for scores in the mid-700s and above for their prime rates. For an auto loan, a score in the upper 600s might get you approved, but a 720+ score will unlock significantly better interest rates. So, when considering "What is a good credit score?", think about your financial goals.

The Benefits of Moving from "Fair" to "Good" and Beyond

Let's put this into perspective. Imagine you're buying a $300,000 home with a 30-year fixed mortgage. With a "Fair" credit score (e.g., 620), you might qualify for an interest rate of 7.5%. Your monthly payment would be around $2,098, and you'd pay approximately $455,422 in total interest over the loan's life. Now, with a "Very Good" credit score (e.g., 760), you might secure a rate of 6.5%. Your monthly payment drops to $1,896, and total interest paid is about $382,410. That's a staggering savings of over $73,000! This vividly illustrates why answering "What is a good credit score?" with action is so financially rewarding.

Achieving and Maintaining Excellence: How to Get a Good Credit Score

Improving your credit score is a marathon, not a sprint, but the effort is well worth it. If you've been asking "What is a good credit score?" and realizing yours isn't quite there yet, here are practical steps to elevate and maintain it:

Practical Steps to Improve Your Credit Score

- Pay All Your Bills On Time, Every Time: This is the golden rule. Set up reminders or automatic payments to ensure you never miss a due date, not just for credit cards and loans, but also utilities, rent, and other recurring bills.

- Keep Your Credit Utilization Low: Aim to use less than 30% of your available credit on each card, and ideally, across all your cards. If you have a $10,000 credit limit, try to keep your balance below $3,000. Paying down balances is one of the quickest ways to see a score improvement.

- Don't Close Old Accounts: The length of your credit history matters. Keeping old, established accounts open (even if you rarely use them, as long as they don't have annual fees) helps boost your average account age.

- Diversify Your Credit Mix (Responsibly): Having a mix of revolving credit (credit cards) and installment loans (mortgage, auto loan, student loan) can be beneficial, but only if you can manage them all responsibly. Don't take out loans you don't need just to diversify.

- Limit New Credit Applications: Only apply for new credit when you genuinely need it. Each hard inquiry can cause a small, temporary dip in your score. Spreading out applications over time is wise.

- Regularly Check Your Credit Report: Obtain free copies of your credit report from AnnualCreditReport.com from each of the three major bureaus (Equifax, Experian, TransUnion). Review them for errors or fraudulent activity and dispute any inaccuracies immediately.

- Consider a Secured Credit Card or Credit-Builder Loan: If you're new to credit or rebuilding, these products can be excellent tools. A secured card requires a cash deposit as collateral, while a credit-builder loan essentially helps you save money while establishing a payment history.

Common Misconceptions About Credit Scores

Navigating the world of credit can be confusing, and several myths persist. Let's debunk a few:

- Checking Your Own Credit Score Harms It: False. Checking your own score results in a "soft inquiry," which does not affect your score. Only "hard inquiries" from lenders when you apply for credit can temporarily lower it.

- Debit Cards Build Credit: False. Debit cards use your own money and are not reported to credit bureaus. Only credit products (loans, credit cards) contribute to your credit history.

- Carrying a Balance Helps Your Credit: False. Paying your credit card balance in full each month is the best practice. Carrying a balance accrues interest and contributes to higher credit utilization, which can harm your score.

- You Only Have One Credit Score: False. As discussed, you have multiple scores from different models (FICO, VantageScore) and different credit bureaus. Lenders also create their own custom scores based on their risk models.

Ultimately, understanding what is a good credit score is the first step toward achieving financial freedom and stability. It's a testament to your financial responsibility and opens doors to better opportunities and significant savings. By consistently practicing good credit habits – paying on time, keeping utilization low, and monitoring your reports – you can build and maintain a strong credit profile that serves you well throughout your life. Remember, your credit score is a dynamic number; a little consistent effort can lead to big rewards.

Comments